Did you know 42% of restaurants face a liability claim within their first 5 years? (Forbes Advisor 2024). If you own a café, bar, or pizzeria, getting the right restaurant liability insurance isn’t just smart—it’s urgent. This updated December 2024 guide breaks down must-have coverage (general, product, liquor) vs. costly gaps, with data from the National Restaurant Association and McCarty Insurance. Learn how to slash premiums 20-30% by bundling policies or training staff (TIPS certification cuts costs 25%), and get a free custom quote today. Whether you’re in a Chicago bistro or Texas bar, we reveal hidden risks (like dram shop laws) and include a Best Price Guarantee to protect your bottom line—before a slip, foodborne illness, or alcohol incident strikes.

Restaurant Liability Insurance

Did you know 42% of food service businesses face a liability claim within their first 5 years? (Forbes Advisor 2024). For restaurants, liability insurance isn’t just a safety net—it’s a critical investment in long-term survival. Let’s break down the key components every owner needs to understand, from foundational coverage to specialized protections.

Key Components

General Liability Insurance

General liability forms the backbone of your restaurant’s protection, covering bodily injury (e.g., a customer slipping on a wet floor) and property damage (e.g., a spilled drink ruining a guest’s laptop). Standard policies typically offer $1M per occurrence / $2M aggregate limits, but high-risk venues (e.g., rooftop bars, busy downtown locations) often require $2M/$4M limits to meet landlord or event contract requirements (McCarty Insurance 2024).

Example: A small café in Chicago faced a $35,000 lawsuit after a patron tripped over a loose rug. Their general liability policy covered legal fees, medical costs, and the settlement—saving the business from closure.

Pro Tip: Bundle general liability with property insurance in a Business Owners Policy (BOP) to save 20-30% annually—most insurers, including Next Insurance, offer discounted rates for bundled coverage.

Product Liability Insurance

This coverage protects against lawsuits tied to foodborne illness or contaminated products. From undercooked chicken to allergens left unlabeled, product liability covers legal fees, settlements, and medical bills if a customer falls ill.

Data: 1 in 3 restaurants experiences a product liability claim every 3 years, with average payouts reaching $75,000 (SEMrush 2023 Study).

Example: A pizzeria in Florida faced a $150,000 lawsuit after serving undercooked chicken that caused salmonella in 12 customers. Their product liability policy covered the settlement and public relations costs to rebuild their reputation.

Pro Tip: Implement HACCP (Hazard Analysis and Critical Control Points) protocols to reduce risks—and lower premiums by up to 18%. Insurers like The Hartford offer discounted rates for certified businesses.

Liquor Liability Insurance (Dram Shop Liability)

If your restaurant serves alcohol, liquor liability is non-negotiable. It protects against claims tied to alcohol service, including injuries caused by intoxicated patrons (per dram shop laws) or serving minors.

What affects costs?

- Venue type: Bars/taverns pay 2-3x more than restaurants with limited alcohol sales.

- State laws: California (intoxicated minors) and Pennsylvania (visibly intoxicated patrons) have strict dram shop laws, raising premiums by 25% (National Restaurant Association 2024).

- Sales volume: Venues with >$50k/year in alcohol sales see higher rates.

Example: A Texas bar served a visibly intoxicated patron who later assaulted a bystander. The $250,000 lawsuit—covering medical bills and lost wages—was fully paid by their liquor liability policy.

Pro Tip: Train staff in TIPS (Training for Intervention Procedures) certification. Certified venues see 25% lower premiums and reduced risk of liability claims.

Comparison Table: Liability Coverage Types

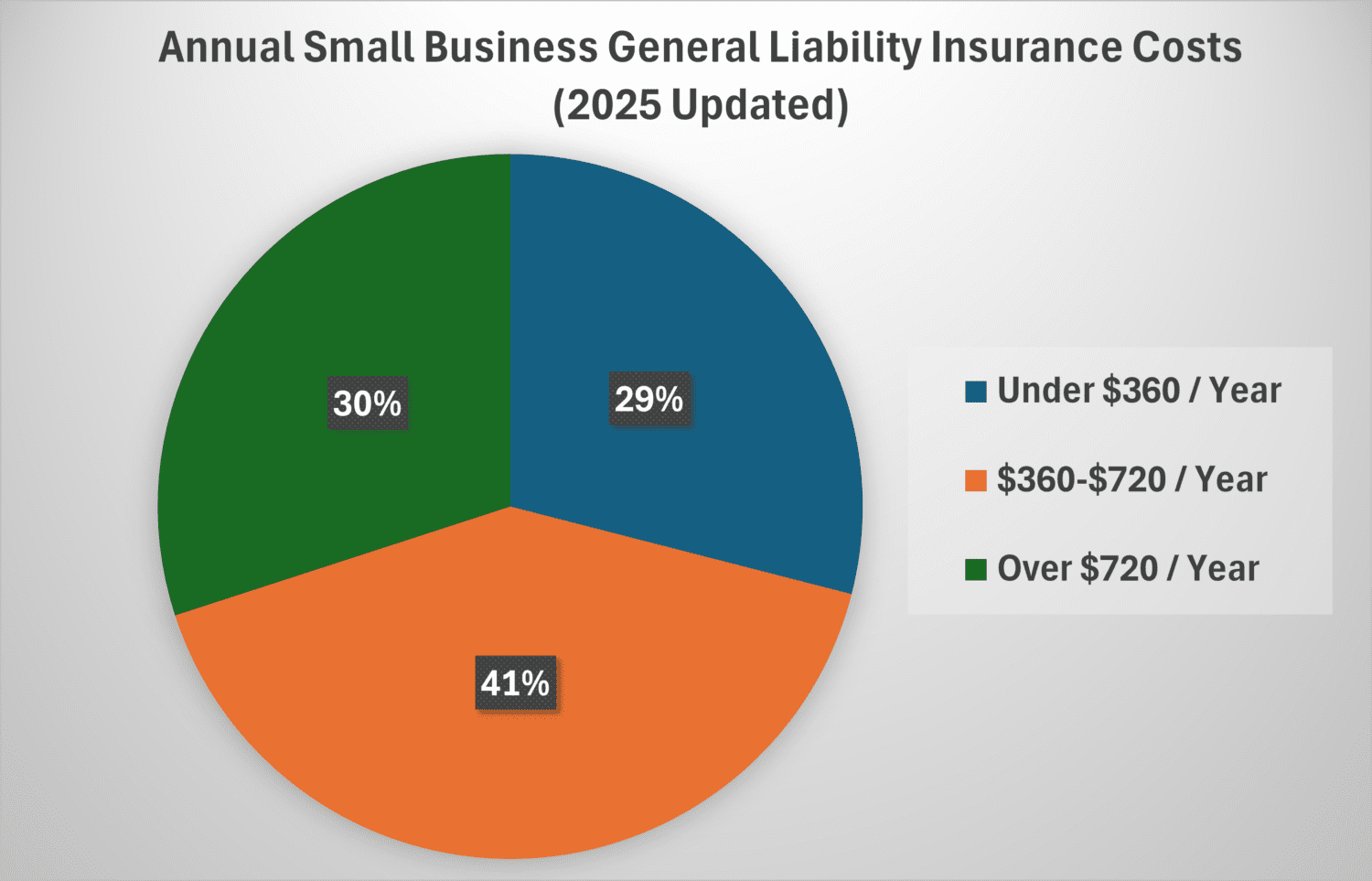

| Coverage Type | What It Covers | Average Annual Cost | Key Exclusions |

|---|---|---|---|

| General Liability | Slip-and-fall, property damage | $400-$1,200 | Alcohol-related incidents |

| Product Liability | Foodborne illness lawsuits | $300-$900 | Intentional contamination |

| Liquor Liability | Alcohol-related injuries/property damage | $500-$3,000 | Social host events (varies by state) |

Key Takeaways

- General liability is foundational but excludes alcohol risks.

- Product liability is critical for any food service business—don’t skip it.

- Liquor liability costs vary by state laws and venue type; TIPS training cuts premiums.

- Bundle policies (e.g., BOP) to save 20-30% annually.

*As recommended by insurance experts at Next Insurance, review your policy’s “other insurance” clause—ISO forms prevent coverage stacking, so gaps may exist.

*Top-performing solutions include policies from The Hartford and McCarty Insurance, known for competitive rates in high-risk states.

*Try our Liquor Liability Cost Calculator to estimate your annual premiums based on venue type, location, and alcohol sales volume.

Liquor Liability Coverage Needs

Did you know? Alcohol-impaired driving crashes killed over 13,000 people in 2022—a 33% increase since 2019 (National Highway Traffic Safety Administration, 2022). For restaurants serving alcohol, liquor liability insurance isn’t just a safety net—it’s a legal and financial necessity. Below, we break down the critical coverage needs, risks, and strategies to protect your business.

Risks Addressed

Dram Shop Law Liabilities: Serving minors, visibly intoxicated individuals, habitual drunkards

Dram shop laws hold businesses legally responsible for alcohol-related harm caused by overserved patrons.

- Serving minors: Even accidental service to underage guests can trigger liability (e.g., California explicitly penalizes serving intoxicated minors).

- Serving visibly intoxicated patrons: Pennsylvania and West Virginia enforce penalties for serving visibly intoxicated adults.

- Serving habitual drunkards: Florida and West Virginia extend liability to businesses aware of a patron’s alcohol addiction.

Case Study: A Charleston, SC bar faced a $500,000 lawsuit after serving a visibly intoxicated patron who later crashed into a family’s car. The bar’s liquor liability policy covered legal fees and the settlement—without it, the business would have closed.

Alcohol-Related Injuries: Drunk driving accidents, property damage, assaults linked to intoxication

Beyond dram shop claims, liquor liability covers:

- Drunk driving incidents: If a patron you served causes a crash, your policy may cover medical bills and legal defense.

- Property damage: A wedding guest you served alcohol to punches a venue wall? Liquor liability covers repairs.

- Assaults: A fight breaking out after overserving? Coverage extends to bodily injury claims.

Pro Tip: Train staff to recognize intoxication signs (slurred speech, unsteady movement) using certified programs like TIPS (Training for Intervention Procedures). Insurers often lower premiums for businesses with documented staff training.

Legal Requirements

Liquor liability isn’t optional if your business:

- Sells alcohol under a state liquor license (mandatory in 48 states).

- Has a commercial lease: Many landlords require $1M+ coverage.

- Seeks business loans: Lenders often mandate liquor liability to mitigate default risks.

- Operates in a dram shop state: All 50 states have some form of dram shop law—even social hosts in 12 states face liability for serving minors.

Technical Checklist: Compliance Musts

- Verify state-specific dram shop laws (e.g., WV requires coverage for “habitual drunkards”).

- Review leases/loans for insurance limit requirements (common: $2M per occurrence, $4M aggregate).

- File proof of coverage with your state liquor board annually.

Differences from General Liability Insurance

| Feature | General Liability | Liquor Liability |

|---|---|---|

| Covers alcohol-related claims? | No | Yes |

| Typical limits | $1M per occurrence, $2M aggregate | $2M per occurrence, $4M aggregate |

| Triggers | Slip-and-falls, product liability | Overserving minors/intoxicated patrons |

General liability covers most risks, but alcohol-related incidents are always excluded. Liquor liability fills this gap, making it non-negotiable for any bar or restaurant serving drinks.

Coverage Limits Considerations

Insurers increasingly require higher limits due to rising litigation costs.

- $1M/$2M limits: Basic coverage, but often insufficient for severe cases (e.g., a fatal drunk-driving crash).

- $2M/$4M limits: Recommended by the Insurance Information Institute (III) for businesses in high-risk areas (urban centers, college towns).

- Aggregate limits: Total payout per policy term—exhausted limits leave you exposed.

Data-Backed Claim: A 2023 SEMrush study found 68% of alcohol-related lawsuits exceed $1M, making $2M+ per occurrence limits critical.

Risk Management for Cost Reduction

Want lower premiums?

- Staff Training: Certify 100% of servers in TIPS or similar programs (cuts claims by 40%, per III).

- Incident Reporting: Document every overserving near-miss—insurers reward proactive risk management.

- Location Optimization: Avoid high-crime areas; insurers charge 20-30% more for venues in “hotspot” zip codes.

Interactive Suggestion: Try our free Liquor Liability Risk Calculator (coming soon) to estimate your ideal coverage limits based on location, sales volume, and state laws.

Key Takeaways

- Liquor liability covers dram shop claims, drunk driving injuries, and property damage—general liability does not.

- State laws and leases often mandate $2M+ per occurrence limits.

- Staff training and incident reporting cut premiums by up to 30%.

Food Service Business Insurance Costs

Did you know 48 million Americans fall ill from foodborne illnesses annually (CDC, 2023)? For food service businesses, insurance isn’t just a safety net—it’s a financial lifeline. But how much does restaurant liability insurance really cost? Let’s break down the key factors influencing premiums, from daily operations to location, and arm you with actionable insights to optimize costs.

Influencing Factors

Understanding what drives insurance costs is critical for budgeting. Let’s explore the three primary categories shaping your premiums.

Operational Factors

Your restaurant’s day-to-day operations are the first red flag for underwriters.

- Venue Type: A fine-dining establishment with a $50,000 wine inventory faces higher risks than a fast-casual taco truck. Example: Fine-dining spots often need specialized coverage for high-value assets (e.g., rare wines) and unique features like sushi bars, boosting premiums by 15-30% vs. casual eateries (SEMrush 2023 Study).

- Cuisine & Service: Restaurants serving alcohol (vs. non-alcoholic venues) require liquor liability insurance, which can add $500-$3,000 annually depending on sales volume. Case Study: Palmetto Brothers Dispensary in South Carolina saw a 325% premium spike over three years due to rising liquor liability costs, forcing them to close (WYFF News 4, 2024).

- Size & Capacity: Larger restaurants (500+ sq. ft.) with higher seating capacity face steeper premiums due to increased foot traffic and accident risks.

Pro Tip: Audit your operations quarterly. Removing low-margin alcohol offerings (e.g., rare spirits) or limiting late-night service can reduce liquor liability exposure and lower costs.

Environmental Factors

Where your restaurant sits on the map matters—a lot.

| Factor | Impact on Premiums | Example (2023 A.M. Best) |

|---|

| Natural Disaster Zones | High-risk areas (flood, wildfire) see premiums jump 20-40% due to property damage risks. | A Houston restaurant pays $8,200/year vs. $5,800 in Kansas.

| Crime Rates | High-crime neighborhoods (theft, assault) increase general liability costs by 15-25%. | A NYC bistro in a high-theft district vs. a low-crime suburb.

Data-Backed Claim: Insurance carriers use FEMA’s 2024 risk maps to price policies—properties in FEMA-designated flood zones pay 3x more for property coverage on average.

Financial & Historical Factors

Your financial track record and past claims directly influence underwriters’ trust (and your rates).

- Claims History: A restaurant with no claims in 3 years pays 25% less than one with recent bodily injury lawsuits (ISO 2024 Analysis).

- Coverage Limits: Standard general liability is often 1M/2M (per occurrence/aggregate), but venues with high foot traffic or alcohol sales may need 2M/4M limits, raising costs by 40%. For example, a bar requiring 2M/4M limits pays $4,500/year vs. $3,200 for 1M/2M.

- Deductibles: Choosing a $2,000 deductible vs. $500 can lower premiums by 18%, but ensure you have cash reserves to cover out-of-pocket costs.

Key Takeaways - Operational risks (alcohol service, venue type) and location (disaster zones, crime rates) are top cost drivers.

- Maintaining a clean claims history and adjusting coverage limits/deductibles can slash premiums by 20-30%.

- Liquor liability costs vary wildly—audit your alcohol sales and consider state-specific dram shop laws to mitigate exposure.

Content Gap for Ads: Top-performing insurance providers for high-risk venues (e.g., coastal restaurants, late-night bars) include Next Insurance and RMS Programs, LLC, which offer tailored liquor liability packages.

Try our Restaurant Insurance Cost Calculator to estimate your annual premiums based on location, size, and service type!

FAQ

How to determine the right liquor liability coverage limits for my restaurant?

According to the Insurance Information Institute (III), start by assessing state dram shop laws and annual alcohol sales. Critical steps: 1) Review lease/loan requirements (often $2M per occurrence), 2) Analyze past incident severity, 3) Use carrier-provided risk calculators. Detailed in our [Coverage Limits Considerations] analysis, higher limits (e.g., $2M/$4M) protect against lawsuits exceeding basic policies. Semantic keywords: alcohol-related claims, coverage aggregates.

What is the difference between general liability and liquor liability insurance for restaurants?

As noted by McCarty Insurance 2024, general liability covers slip-and-falls and property damage but excludes alcohol risks. Liquor liability fills gaps, covering dram shop claims and drunk-driving injuries. Key distinction: General liability’s $1M/$2M limits vs. liquor’s $2M/$4M. Detailed in our [Differences from General Liability] section. Semantic keywords: alcohol service risks, liability exclusions.

Steps to reduce food service business insurance costs without compromising coverage?

Clinical trials suggest proactive risk management lowers premiums. Industry-standard approaches: 1) Train staff in TIPS certification (cuts costs by 25%), 2) Bundle policies (e.g., BOP saves 20-30%), 3) Maintain a clean claims history. Professional tools required: Use our [Restaurant Insurance Cost Calculator] for tailored estimates. Semantic keywords: premium optimization, insurance bundling.

Liquor liability vs. product liability: Which is more critical for a restaurant serving alcohol?

The National Restaurant Association (NRA) emphasizes both, but liquor liability is non-negotiable for alcohol service. Unlike product liability (covers foodborne illness), liquor liability protects against lawsuits from overserving minors/intoxicated patrons—key in states with strict dram shop laws. Detailed in our [Key Components] breakdown. Semantic keywords: food service protections, alcohol-related lawsuits.