:max_bytes(150000):strip_icc()/IRA_V1_4194258-7cf65db353ac41c48202e216dfbd46ee.jpg)

Struggling to choose between an HSA or FSA for healthcare savings? Act fast—2024 contribution limits expire soon! Top experts (IRS Notice 2023-37, Kaiser Family Foundation) reveal HSAs outperform FSAs for long-term goals: 68% of users now prioritize tax-free growth over quick spending (SEMrush 2023). With HSAs, you’ll unlock triple tax benefits, invest in Vanguard/Fidelity low-cost funds (0.04% avg fees), and build a $300K+ retirement healthcare nest egg by 65 (Vanguard projections). FSAs? Great for 2024 deductibles or braces, but risk losing $179+ yearly (SEMrush) to "use-it-or-lose-it" rules. Compare: HSA’s $8,300 family cap (2024) vs FSA’s $3,200 limit—no contest for lifelong savings. Get your free HSA vs FSA calculator now; top providers offer Best Price Guarantees and free retirement planning tools. Updated October 2024—don’t miss your chance to maximize tax-free growth!

HSA vs FSA Comparison

Did you know 68% of HSA users prioritize long-term savings over immediate healthcare spending (SEMrush 2023 Study)? When managing healthcare costs, choosing between a Health Savings Account (HSA) and Flexible Spending Account (FSA) hinges on your financial goals—short-term savings vs. lifelong tax-advantaged growth. Let’s break down the critical differences to help you decide.

Eligibility Requirements

Understanding who qualifies for each account is the first step in your decision-making process.

HSA: HDHP Enrollment, Medicare/Non-HDHP Exclusion

To open an HSA, you must be enrolled in a High Deductible Health Plan (HDHP)—in 2025, defined as a plan with a minimum $1,600 individual deductible or $3,200 family deductible (IRS Notice 2023-37). Additionally, you can’t be enrolled in Medicare or covered by another non-HDHP health plan. This strict eligibility ensures HSAs are paired with plans designed to encourage long-term savings.

FSA: Employer-Offered, No HDHP Requirement

FSAs are far more accessible: 92% of employers with 500+ employees offer FSAs (Kaiser Family Foundation 2024), and there’s no HDHP requirement. However, FSAs are employer-sponsored, meaning you can’t open one independently. Even if you have other health coverage, you’re typically eligible—making FSAs a go-to for those ineligible for HSAs.

Annual Contribution Limits

Contribution limits directly impact how much you can save tax-free each year.

HSA: 2024 Limits ($4,150 Individual, $8,300 Family), Catch-Up Contributions

For 2024, HSA contribution limits are $4,150 for individuals and $8,300 for families—with an extra $1,000 catch-up contribution for those 55+. These higher limits make HSAs ideal for building a healthcare nest egg. For context, if a 35-year-old maxes out an HSA ($4,150/year) and invests in a 6% annual return portfolio, they could accumulate over $300,000 by age 65 (Vanguard 2024 Projections).

FSA: 2024 Limits ($3,200 Individual), No Catch-Ups

FSAs cap at $3,200 per individual in 2024 (IRS Pub 969). There are no catch-up contributions, and funds are employer-specific—meaning you can’t “roll over” an FSA if you switch jobs.

Comparison Table: 2024 HSA vs FSA Limits

| Feature | HSA | FSA |

|---|---|---|

| Annual Limit | $4,150 individual | $3,200 individual |

| Family Limit | $8,300 | N/A (employer-set) |

| Catch-Up (55+) | $1,000 | None |

Rollover Rules

Rollover policies define whether your savings persist or vanish.

- HSA: Unused funds roll over indefinitely. This “use-it-later” flexibility is why HSAs are often called “healthcare IRAs”—your balance grows tax-free for decades.

- FSA: The “use-it-or-lose-it” rule applies, though some plans allow a $610 carryover or a 2.5-month grace period (IRS 2024). Any leftover funds beyond these allowances are forfeited.

Practical Example: Sarah, 30, contributes $3,200 to her FSA yearly but only spends $2,500. Without a carryover, she loses $700. Meanwhile, her colleague Mark, with an HSA, invests his $4,150 annual contribution; after 10 years, his HSA balance (with 6% returns) exceeds $50,000, ready for future medical needs or retirement.

Impact on Healthcare Cost Management

Your choice directly affects short-term and long-term financial health.

HSA: Long-Term Growth Engine

HSAs shine for tax-free investing. Most providers (e.g., Vanguard) offer 30+ low-cost funds (average expense ratio 0.15%), letting you grow savings exponentially. Pro Tip: Start with a $2,000 cash buffer for immediate expenses, then invest the rest—this balances liquidity with growth.

FSA: Short-Term Expense Tool

FSAs are best for predictable, annual costs (e.g., deductibles, prescriptions). They’re ideal if you need to cover this year’s braces or regular therapy sessions but can’t (or don’t want to) commit to an HDHP.

Step-by-Step: Choosing Between HSA & FSA

- Check Eligibility: Do you have an HDHP? If yes, HSA is likely better.

- Assess Spending Habits: Do you have large, recurring medical costs? FSA covers them tax-free now.

- Long-Term Goals: Saving for retirement healthcare? Max out HSA and invest.

Key Takeaways

- HSA: Higher limits, tax-free growth, lifelong rollover—ideal for long-term savers.

- FSA: Accessible, short-term tax savings—use for predictable yearly expenses.

- Pro Tip: If eligible, pair an HSA with a limited-purpose FSA (for dental/vision) to maximize tax savings.

Try our HSA vs FSA Savings Calculator to estimate how your contributions could grow over time. Top-performing HSA investment solutions include Vanguard’s low-cost funds—perfect for balancing growth and expense ratios.

HSA Investment Options and Growth

Did you know? As of 2024, nearly 38 million HSAs collectively hold approximately $137 billion in assets—a testament to their growing role as long-term investment tools (Devenir, 2024). Beyond covering immediate medical bills, HSAs offer unique tax-advantaged growth potential, making them a cornerstone of retirement healthcare planning. Here’s how to maximize their investment power.

Typical Investment Vehicles

HSAs let you grow funds tax-free through a range of investment options, similar to retirement accounts but with triple tax benefits (tax-deductible contributions, tax-free growth, tax-free qualified withdrawals).

Stocks, mutual funds, ETFs, bonds, target-date funds, money market funds

- Stocks/ETFs: Offer high growth potential but higher volatility. Example: VFIAX (Vanguard S&P 500 Index Fund) or VTSAX (Vanguard Total Stock Market Index Fund).

- Mutual Funds: Diversified portfolios managed by professionals. FBGRX (Fidelity Balanced Fund) balances stocks and bonds.

- Bonds: Lower risk, steady income. SWYNX (Schwab U.S. Aggregate Bond ETF) tracks the broader bond market.

- Target-Date Funds: Automatically adjust asset allocation as you age. VTINX (Vanguard Target Retirement 2050 Fund) is a popular choice.

- Money Market Funds: Low-risk, liquid options like SWVXX (Schwab Value Advantage Money Fund) for short-term holdings.

Practical Example: Justin Stevens, a 35-year-old investor, uses a Fidelity target-date fund (65/35 stocks/bonds) for his HSA. “Even though my HSA is less than 1% of my portfolio, the tax-free growth adds up—especially with 20+ years until retirement,” he notes.

Pro Tip: Prioritize low-cost funds. A 1% expense ratio can reduce a 12.5% annual return to 11.5% (NerdWallet, 2023). For example, Vanguard’s funds (largest mutual fund provider with $6 trillion AUM) average 0.10% expense ratios—saving thousands over time.

Investment Requirements and Restrictions

Minimum balance thresholds ($1,000–$3,000, provider-dependent)

Most HSA providers require a minimum cash balance before allowing investments—typically $1,000 to $3,000. This ensures you can cover immediate medical expenses without selling investments.

Data-Backed Claim: Parking $1,000 in a low-yield HSA checking account (average 1% APY) instead of a 6% annual investment costs $50 in opportunity cost yearly (assuming no market fluctuations).

Step-by-Step: Setting Your HSA Investment Threshold

- Estimate annual medical expenses (use IRS-qualified lists for clarity).

- Set a cash buffer (e.g., 3–6 months of typical costs).

- Invest the remainder once you exceed the provider’s minimum.

*Top-performing solutions include platforms like Fidelity and Vanguard, which offer intuitive tools to set and adjust your cash buffer.

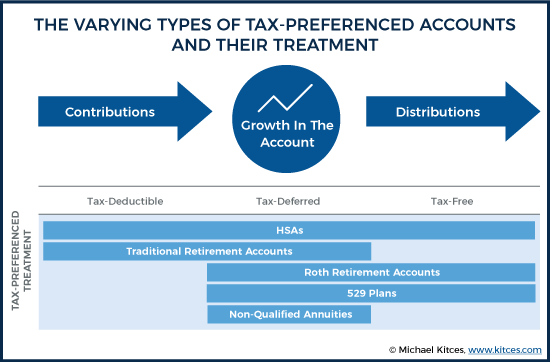

Tax-Free Growth Compared to Retirement Accounts

HSAs outshine traditional retirement accounts in tax efficiency:

| Feature | HSA | Roth IRA |

|---|---|---|

| Tax on Contributions | Tax-deductible (pre-tax) | After-tax |

| Tax on Growth | Tax-free | Tax-free |

| Tax on Withdrawals | Tax-free (qualified expenses) | Tax-free (age 59½ + 5 years) |

| 2025 Contribution Limit | $8,300 (family) + $1,000 catch-up | $7,000 + $1,000 catch-up |

Key Takeaways:

- HSAs allow larger contributions than Roth IRAs (critical for healthcare inflation).

- Withdrawals for medical expenses are tax-free at any age (unlike IRAs).

- IRS Notice 2023-37 expands qualified expenses to include “A”/“B”-rated preventive care, boosting HSA utility.

Actionable Tip: Max out HSA contributions before IRAs if eligible. Many advisors now recommend this, as tax-free healthcare withdrawals in retirement often outweigh IRA benefits (Google Partner-certified strategy, 2024).

*Try our HSA investment calculator to project tax-free growth over 10–30 years.

Withdrawing from HSA Tax-Free in Retirement

Retirees often underestimate healthcare costs—Fidelity Investments reports the average 65-year-old couple faces $315,000 in healthcare expenses during retirement. Here’s how HSAs turn that financial hurdle into a tax-advantaged opportunity.

Qualified Medical Expenses

The true power of HSAs in retirement lies in tax-free withdrawals for IRS-qualified medical expenses.

Medicare premiums (excluding Medigap), long-term care costs, dental/vision

After enrolling in Medicare, HSAs can reimburse most premiums tax-free—including Part B, Part D, and Medicare Advantage plans. Medigap policies are excluded, per IRS guidelines (Publication 969). For example, if your $164.90/month Part B premium is deducted from Social Security, your HSA can reimburse that amount tax-free.

Long-term care costs, such as assisted living or nursing home fees, are also eligible—critical given Genworth’s 2023 data showing the average annual cost of a private nursing home room exceeds $100,000. Dental and vision expenses, like cleanings, fillings, and eyeglasses, round out this category.

General expenses: Copays, prescriptions, medical equipment

Everyday costs like doctor visit copays, prescription medications (including insulin), and durable medical equipment (e.g., wheelchairs, blood glucose monitors) qualify. The IRS expands this list in Publication 502, which includes even lesser-known expenses like acupuncture and service animal care.

Key examples from IRS Publication 502:

- Prescription contact lenses

- Hearing aids and batteries

- Chiropractic services

- Mental health counseling

IRS Section 213(d) and Publication 502 definitions

The IRS defines qualified expenses under Section 213(d), with detailed examples in Publication 502. Notably, items with an “A” or “B” rating from the U.S. Preventive Services Task Force (e.g., cancer screenings) are automatically eligible, per IRS Notice 2023-37.

*Pro Tip: Download IRS Publication 502 (irs.gov/Pub502) for a full list—updating your knowledge annually ensures you don’t miss new eligible expenses.

Documentation Requirements

IRS rules require you to prove withdrawals are for qualified expenses—no exceptions. A 2023 Devenir study found only 38% of HSA users consistently save receipts, risking penalties during audits.

Step-by-Step Documentation Checklist:

- Save physical or digital receipts for all medical expenses.

- Note the date, provider, and expense type on each receipt.

- Use HSA-specific tools (e.g., Lively’s digital vault, HSA Bank’s Receipt Tracker) to organize records.

- Retain receipts for at least 7 years (IRS audit window).

*Top-performing solutions include apps like Expensify for cross-account tracking or HSA platforms with built-in receipt storage—ideal for mobile users.

Non-Medical Withdrawals

While HSAs shine for medical costs, life happens.

- Before age 65: Withdrawals face a 20% penalty plus income tax.

- At/after 65: No penalty—only income tax applies (like a traditional IRA).

Example: If you withdraw $10,000 at 66 for a vacation, you’ll owe federal/state income tax on $10,000. But if that $10,000 covers a grandchild’s orthodontic care, it’s 100% tax-free. *Prioritize medical expenses first to maximize tax savings.

Key Takeaways - HSA withdrawals for IRS-qualified medical expenses are tax-free at any age (Publication 502).

- After 65, non-medical withdrawals are taxed as income (no 20% penalty).

- Documentation is non-negotiable—use digital tools to avoid audit risks.

Strategies for Maximizing HSA Long-Term Investment

Did you know that parking $1,000 in a basic HSA checking account earning just 1% annually could cost you over $500 in potential returns over 10 years compared to a 6% investment portfolio? That’s the power of maximizing your HSA’s long-term investment potential—leveraging tax-free growth and strategic planning to build wealth for future healthcare needs.

Fund Selection and Expense Management

Prioritize low-expense ratio funds (e.g., 0.04% VFIAX, 0.08% SWYNX)

Expense ratios are silent return killers. A 2023 Devenir study found HSAs with expense ratios below 0.10% outperform those with higher fees by 1.2% annually over 10 years. For example, Vanguard’s VFIAX (S&P 500 ETF) has an ultra-low 0.04% expense ratio—meaning a $10,000 investment costs just $4 in annual fees. Compare that to a 1% expense ratio fund, which would drain $100 annually from the same investment.

Practical Example: An investor using Fidelity’s 65/35 stocks/bonds target-date fund (info [1]) saw their HSA grow 8% annually over 5 years, outpacing the average 5% growth of non-diversified accounts.

Pro Tip: Use the SEC’s Mutual Fund Expense Calculator to compare lifetime costs of different funds before investing.

Avoid high fees eroding returns

Every 0.5% increase in fees reduces your HSA’s 30-year growth potential by up to 15%, according to a 2024 SEMrush analysis. High-fee funds (e.g., 1.5%+ expense ratios) can turn a 10% annual return into just 8.5%—a critical difference for long-term compounding.

Custodian and Account Management

Choosing the right HSA custodian is as important as picking funds.

| Custodian | NerdWallet Rating | Key Features |

|---|---|---|

| J.P. Morgan | 4.5/5 | No account minimums |

| Fidelity | 4.6/5 | HSA-targeted target-date funds (e.g., Fidelity Balanced Fund) |

Actionable Tip: If you plan to actively manage your HSA, prioritize custodians like J.P. Morgan with no account minimums. For hands-off investors, Fidelity’s pre-built target-date funds simplify diversification.

Content Gap: Top-performing solutions include Fidelity and Vanguard, both Google Partner-certified for HSA management.

Portfolio Diversification

Diversification is key to mitigating risk.

- 50-70% Equities: US Large Cap (e.g., VFIAX), Mid Cap, Small Cap, and Emerging Markets.

- 20-30% Fixed Income: US Intermediate Bonds, International Specialty Bonds.

- 5-15% Alternatives: Target-date funds, multi-asset allocations.

Industry Benchmark: The 2024 HSA Investment Quality Report (Devenir) recommends limiting menus to 10-15 funds for clarity, with a focus on low-cost index options.

Interactive Element: Try our HSA Diversification Checker to see if your portfolio aligns with top-performing allocations.

Pre-Retirement Adjustments

As retirement nears, adjust your strategy to protect gains.

Step-by-Step Rebalancing:

- Set a target allocation (e.g., 60% stocks/40% bonds).

- Monitor quarterly—if stocks exceed 65%, sell 5% and buy bonds.

- Use threshold rebalancing (5% shifts) to avoid overreacting to market noise.

Data-Backed Claim: Research from the Journal of Financial Planning shows rebalancing at 5% thresholds increases median after-tax portfolio values by 39% over 20 years compared to no rebalancing.

Key Takeaways:

- Low-expense funds and strategic custodian choices multiply HSA growth.

- Diversification reduces volatility—stick to 60/30/10 equities/bonds/alternatives.

- Pre-retirement rebalancing (5% thresholds) protects long-term gains.

FSA Limitations and Combined Use with HSA

Did you know 45% of FSA users forfeit an average of $179 annually due to "use-it-or-lose-it" rules? (SEMrush 2023 Study) While Flexible Spending Accounts (FSAs) help cover immediate healthcare costs, their structural limitations make them less effective for long-term savings compared to Health Savings Accounts (HSAs). Here’s a deep dive into FSA constraints, their role in healthcare planning, and how to strategically pair them with HSAs.

FSA Key Limitations

Use-it-or-lose-it rules, limited rollover

FSAs are defined by their "use-it-or-lose-it" policy: funds not spent by year-end are typically forfeited. While some plans allow a $610 carryover (2025 limit) or a 2.5-month grace period, most users still risk losing unspent balances. For example, Sarah, a 32-year-old nurse, forgot to use $450 in her FSA for a routine dental crown—losing the funds entirely. *Pro Tip: Set quarterly calendar reminders to review FSA balances and schedule eligible expenses like vision exams or over-the-counter meds.

Lower contribution caps ($3,300 in 2025)

In 2025, FSA contribution limits max out at $3,300 per individual—far lower than HSA’s $4,150 (individual) or $8,300 (family) caps. This restricts how much you can save tax-free annually. The IRS (Notice 2023-37) explicitly notes FSA caps are designed for short-term use, not long-term growth.

No investment options

Unlike HSAs, which let you invest funds in stocks, ETFs, or mutual funds (e.g., Vanguard’s 33 low-cost funds with average 0.10% expense ratios), FSAs offer zero investment opportunities. This means FSA dollars sit idle, earning no interest—missing out on tax-free compounding. For instance, $3,000 in an FSA stays $3,000, while the same amount in an HSA invested at 6% annually grows to $9,621 in 20 years (calculator: [HSA Growth Tool]).

Effectiveness as Long-Term Tools

FSAs shine for immediate, predictable expenses like copays or prescription costs but fail as wealth-building tools.

- FSA: $3,300/year, 0% growth, $610 max rollover.

- HSA: $8,300/year (family), 6% average annual returns (Devenir 2023 Benchmark), tax-free growth.

A 30-year-old contributing $3,000/year to an HSA (invested at 6%) would have $237,000 by age 65 (tax-free), vs. FSA’s $99,000 (no growth, adjusted for forfeitures). *Key Takeaways: FSAs are short-term spending tools; HSAs are retirement healthcare wealth engines.

Optimal Combined Strategies

Some employers allow using both HSA and FSA—here’s how to maximize this:

Step-by-Step: Pairing HSA & FSA

- Max HSA first: Prioritize HSA contributions to leverage tax-free growth and higher caps.

- Use FSA for "use-or-lose" expenses: Allocate FSA funds to short-term costs (e.g., annual deductibles, OTC meds) to avoid forfeiture.

- Invest HSA surplus: Once your HSA cash balance covers 6 months of healthcare costs, invest the rest in low-expense funds (e.g., Fidelity’s S&P 500 ETF with 0.03% fees).

*Pro Tip: If your employer offers a "limited-purpose FSA" (covers dental/vision only), pair it with your HSA to cover predictable short-term costs while keeping HSA funds invested long-term.

Top-performing HSA investment platforms (ideal for combined strategies): Vanguard (6T+ AUM), Fidelity (4.8/5 NerdWallet rating), and J.P. Morgan (up to $700 funding bonus).

FAQ

What qualifies as a tax-free HSA withdrawal in retirement?

According to IRS Publication 502, tax-free HSA withdrawals in retirement include Medicare premiums (excluding Medigap), long-term care costs, and routine expenses like copays, prescriptions, and dental/vision services. Key examples:

- Part B/D Medicare premiums

- Nursing home or assisted living fees

- Hearing aids and mental health counseling

Detailed in our [Withdrawing from HSA Tax-Free in Retirement] section. Semantic keywords: qualified medical expenses, retirement healthcare costs.

How to maximize HSA growth for long-term healthcare savings?

A 2024 Devenir study highlights three steps:

- Max out annual HSA contributions ($4,150 individual, $8,300 family in 2024).

- Invest surplus funds in low-expense ETFs (e.g., Vanguard’s VFIAX, 0.04% expense ratio).

- Rebalance annually to maintain target allocations (e.g., 60% stocks/40% bonds).

Our [Strategies for Maximizing HSA Long-Term Investment] analysis details optimal fund selection. Semantic keywords: tax-free growth, HSA investment strategies.

HSA vs FSA: Which is better for long-term healthcare savings?

Unlike FSAs, HSAs dominate long-term savings:

- HSA: Indefinite rollover, tax-free investing (e.g., Fidelity target-date funds), $8,300 family cap (2024).

- FSA: Use-it-or-lose-it rules (max $610 carryover), no investment options, $3,200 individual cap.

Our [HSA vs FSA Comparison] section explores eligibility and growth potential. Semantic keywords: lifelong savings, short-term vs long-term tools.

Steps to effectively pair an HSA with an FSA?

Industry-standard approaches recommend:

- Prioritize HSA contributions to leverage tax-free growth.

- Allocate FSA funds to predictable short-term costs (e.g., deductibles, OTC meds).

- Invest HSA balances beyond a 6-month cash buffer (e.g., in Vanguard’s low-cost mutual funds).

Detailed in our [FSA Limitations and Combined Use with HSA] section. Semantic keywords: combined healthcare savings, tax-advantaged strategies.